Unknown Facts About Retirement Income Planning

Table of ContentsThe Buzz on Retirement Income PlanningThe Best Strategy To Use For Retirement Income PlanningGetting The Retirement Income Planning To WorkRetirement Income Planning Can Be Fun For Everyone

A retirement income planning is a year through year timeline that shows you where your retirement life revenue will definitely arise from. It may be performed on a slab of graph newspaper, or rather quickly in an Excel spread sheet (or another spread sheet course). Here are actually four easy measures you may make use of to make one.Expand this projection with lifespan expectancy. You can observe an example retirement earnings program on the dining table at the end of this write-up. Make cavalcade headings for every thing you will definitely include in it. Make use of the listed here to establish what things to add. Add rows for every source of preset earnings such as: Program the quantity beginning in the year/age you consider to begin benefits and continue this expectation of life.

Show the amount beginning in the year/age your partner will start perks and also continue it with their life span. If there is actually a grow older or health difference between the 2 of you bear in mind that upon the initial death, the surviving spouse always keeps the much larger of their personal Social Safety or even their husband or wife's.

A distinct column is actually used for each resource of pension plan income. In some instances, the funds from retired life accounts, pension accounts, as well as Social Safety benefits modify located on when you pick to begin the distributions.

7 Easy Facts About Retirement Income Planning Shown

A distinct pillar is actually utilized for each and every source of pension plan profit. If married, make certain you make up the pension account survivor alternative that was actually chosen. Input this merely if you have an allowance that will certainly pay you a guaranteed lowest volume beginning at a certain age or date, with the payment continuing for lifestyle, shared lifestyle, or even for a collection time period of opportunity.

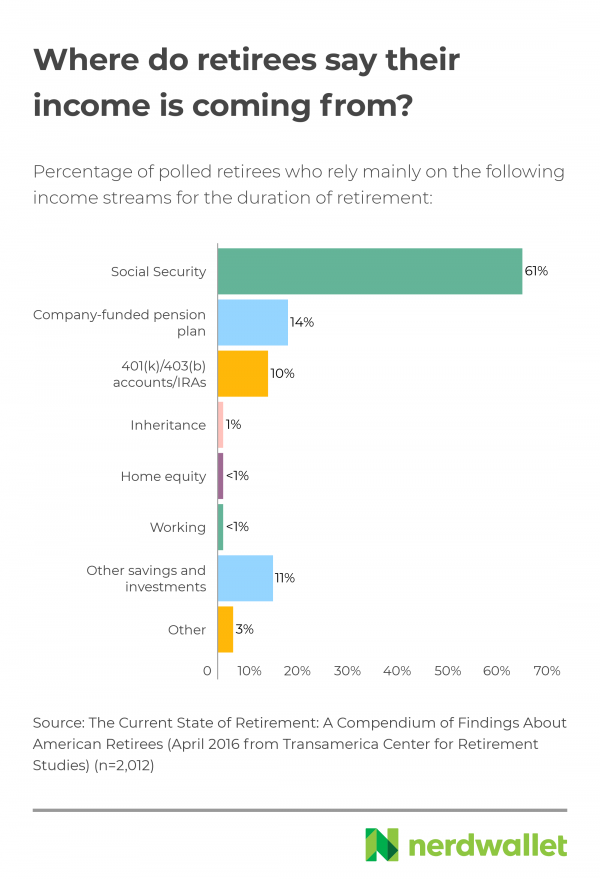

Carry out not input financial investment revenue sources such as dividends, welfare, or resources gains. Rather, you will certainly use your retirement life profit planning to calculate the amount of you are going to need to have to withdraw coming from your economic accounts. When it pertains to withdrawals, take a look at the 1,000-Bucks-a-Month Policy to reverse-engineer the amount of you need to have to conserve for retired life linked here - retirement income planning.

Listing items such as a mortgage loan that might be actually paid for off in a couple of years in a different cavalcade. In the instance at the end of the page, you view the home loan will certainly be actually settled halfway by means of 2025, to ensure year the total annual mortgage repayment is actually half what it was actually the year just before, as well as then that expense disappears.

About Retirement Income Planning

The following year they will definitely have a lot more Social Safety and security income as well as determined they would just require concerning a $15,000 Individual retirement account drawback. Next, your retirement profit plan should calculate the space, which is a deficiency to be actually removed coming from cost savings, or even a surplus readily available to be actually deposited to savings.

If this "Space" is an unfavorable amount, this is what you would certainly need to remove from discounts and financial investments to have your intended retired life way of living. If the "Gap" is an excess at that point you have actually good enough taken care of incomes to fulfill your desired retirement way of living as well as could possibly contribute to cost savings or possibly invest a bit a lot more.

A non-traded REIT is a type of realty assets that permits you to commit in an expertly managed collection of commercial realty. This is actually a non-liquid asset that financiers generally keep for the relation to the trust up until it is liquidated due to the management group. Because of this, it is actually various you can check here coming from publicly-traded REITs, which can be actually dealt on public markets.

"Non-traded REITS are actually certainly not influenced by day-to-day cost volatility as top article is actually the situation with publicly-traded REITs," points out Haworth. Possible to produce revenue from genuine estate without having to be liable for handling the residential or commercial properties.

Some Known Details About Retirement Income Planning

A routine stream of profit (in most sorts of non-traded REITs). Variation for a profile comprised primarily of shares as well as connects. Typically have high control as well as purchase charges. Non-traded REITs possess no assets; you're secured for the regard to the REIT or even subject to charges for early drawback.

This is a fundamental income source for many people. When you make a decision to take it might have a huge influence on your retirement life. It could be tempting to claim your perk as very soon as you're qualified for Social Securitytypically at grow older 62. Yet that may be an expensive action.

(FRA ranges coming from 66 to 67, depending upon the year in which you were actually birthed.) Locate out your full old age, as well as deal with your financial expert to look into exactly how the timing of your Social Protection perk matches your general planning. Although pensions used to be typical, they aren't a great deal any longer.